Your Ultimate Guide to the SEC-mandated T+1 Settlement Cycle

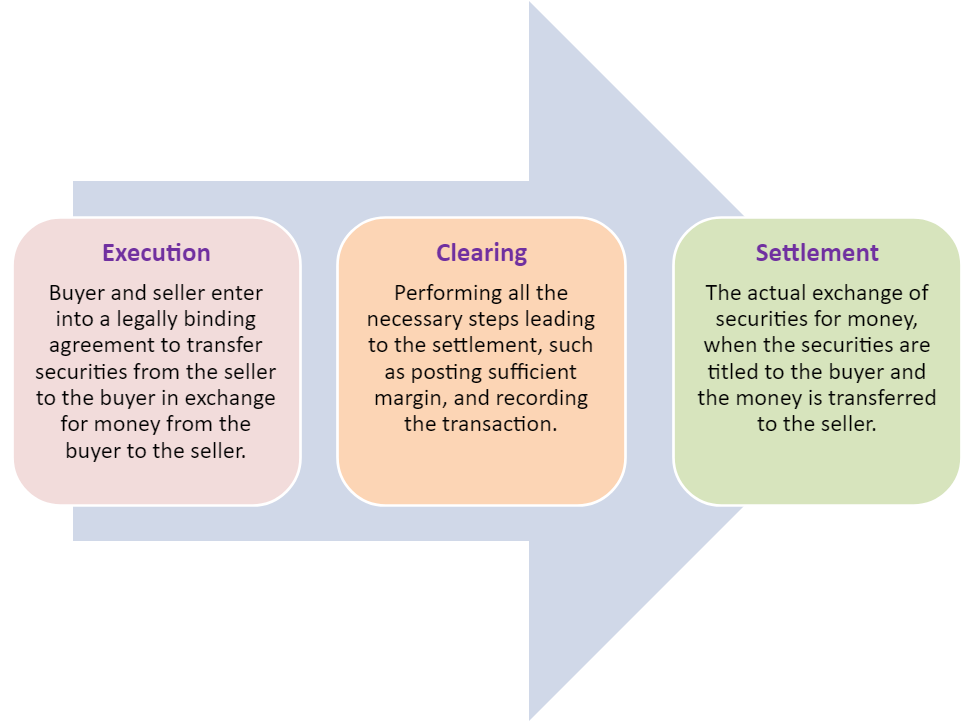

The SEC has notified a new rule which mandates a T+1 settlement cycle under the Securities Exchange Act of 1934. This includes most securities transactions, with the exception of securities transactions that have been exempt from the standard settlement cycle (such as security-based swap transactions).

This move has come after the excess volatility in the financial markets during the start of the coronavirus pandemic and various “meme stock” events further confirmed the belief that the market needed to move towards shorter settlement cycles (from T+2 settlement to T+1 settlement).

A shorter settlement cycle is likely to have several benefits such as reducing liquidity risk, reducing credit risk, and lesser market risk.

As noted by SEC chairman Gary Gensler, “[a T+1 settlement cycle will] make our market plumbing more resilient, timely, orderly, and efficient.”

Other countries such as China and India have already moved towards a T+1 settlement cycle which bolsters the argument that a T 1 settlement cycle is necessary.

Let’s take a look at what the new regulation entails and some of the possible implications for industry players

.

What is the new rule?

The Securities Exchange Act Rule 15c6-1 was amended on February 15, 2023.

According to the amended rule:

- Standard Settlement Cycle will be Shortened to T+1

Earlier, Rule 15c6-1(a) mandated that the majority of broker-dealer transactions involving securities must be settled within two business days after the trade date (T+2), unless the parties have explicitly agreed otherwise at the time of the transaction.

Now, the revised version of the Rule states that most broker-dealer transactions will need to follow a T+1 settlement timeline. However, parties can follow a different timeline through mutual agreement.

Certain transactions, such as those involving government securities, municipal securities, commercial paper, bankers’ acceptances, commercial bills, and exempted securities, will remain excluded from the amended rule.

Also, the standard settlement cycle (T+1) will exclude non-listed limited partnership interests, security-based swaps, and securities that the SEC has exempted through a specific order.

- Settlement Cycle for Firm Commitment Underwritten Offerings Priced After 4:30 p.m. ET will be shortened from T+4 to T+2

Earlier, Rule 15c6-1(c) allowed firm commitment underwritten offerings priced after 4:30 p.m. ET to settle with a T+4 settlement cycle. The SEC has now amended this rule and shortened the standard settlement cycle for these offerings from T+4 to T+2, including most equity and equity-linked offerings that are priced after market close.

Although the SEC had originally proposed to eliminate the longer permitted settlement cycle for firm commitment underwritten offerings, it is convinced by SIFMA’s comments that a T+1 standard settlement (with the parties’ express agreement for an extended settlement date) would not be sufficient to prevent securities transactions priced after 4:30 p.m. ET from failing to settle.

The longer settlement cycle is allowed since unforeseen issues can arise relating to legend removal, transfer agents, non-US parties, medallion guarantees, and so on.

- Same-Day Affirmations are Mandatory

The SEC’s new Rule 15c6-2(a) will require broker-dealers to take one of two actions. Firstly, they must either create written agreements with the relevant parties, like investment managers and bank custodians acting on behalf of a broker-dealer’s customer.

Alternatively, they must establish and uphold written policies and procedures that are reasonably designed to guarantee timely completion of allocations, confirmations, and affirmations, ideally by the end of the trade date and as quickly as technology allows.

If a broker-dealer selects the option to create written policies and procedures under new Rule 15c6-2(a), these policies and procedures must conform to specific criteria. These include outlining applicable technology systems, operations, and processes, as well as monitoring the rates at which allocations, confirmations, and affirmations are completed.

- Investment Advisers will need to Maintain Records

Investment Advisers will need to follow amended Rule 204-2(a)(7)(iii) of the Investment Advisers Act of 1940. This rule requires them to maintain records of each allocation, confirmation, and affirmation related to transactions which come under Rule 15c6-2(a).

These records must include a date and time stamp for each communication, indicating when it was sent or received. To meet this requirement, advisers must keep originals of confirmations and copies of allocations and affirmations. However, they are allowed to maintain these records electronically, provided that the storage meets certain conditions.

When is the T+1 settlement cycle being implemented?

The new T+1 settlement cycle will be enforced from May 28, 2024.

There has been some pushback to such an early enforcement date.

Commissioners Hester Peirce and Mark Uyeda dissented regarding the proposed implementation date. Commissioner Hester Peirce advocated for an implementation date of September 3, 2024, which is the first business day after Labor Day 2024. She argued for this timeline to permit additional time for industry coordination and testing.

What will be the possible implications of a T+1 settlement cycle?

A T+1 settlement cycle is a daunting task for industry actors since the timeline has effectively been halved.

Market participants, including but not limited to clearing houses, broker-dealers, and investment advisors, will need to begin taking action promptly to ensure a seamless transition to the T+1 settlement cycle and compliance with the other new or revised rules by May 28, 2024.

A T+1 settlement cycle leaves much less room for error.

Shortening the settlement cycle to T+1 requires mitigating operational risks. Manual processes will be particularly strained, and automation will be necessary for a T+1 environment to minimize exception management and reduce risk.

Outdated technologies such as fax machines need to be replaced with more automated tools that have built-in operational controls, while staff focus on managing exceptions and correcting transactions. Additionally, firms should investigate the root causes of errors and update obsolete or outdated processes to prevent similar errors in the future.

Wrapping Up

Overall, the shortening of the settlement cycle is a welcome and timely move by regulators. Technological advancements have made it possible for the market to move to a shorter settlement cycle.

An added advantage is that Canada is also moving to T+1 settlement which means that the two markets will remain in sync.

A shortened settlement cycle will be more efficient and it is expected to pave the way for a more stable and surer financial system.