TOP 5 FINTECH TRENDS BACKED BY AUGMENTUM FINTECH – PART 2

In part 1 we explored Augmentum’s backing of AI- powered fintech trends. However AI is just one part of fintech transformation. In this part we explore three other key trends: Embedded Finance, regtech, and payment innovations driving the future of global commerce.

Read on to learn more about the next fintech trends backed by Augmentum

3) Embedded Finance and Open Banking: Key to seamless Financial Access

Embedded finance is enabling every business to become a fintech company by integrating financial offerings into non-financial platforms such as e-commerce, ride-sharing, and social media. It enables users to access financial services without visiting a traditional bank, making finance frictionless and invisible, thereby transforming customer experience.

Embedded finance is not a new trend though and has existed for years through offerings such as airline co-branded credit cards, retailer financing, and in-app payments for ride-sharing services like Uber.

So What’s Changing Now?

Well, embedded finance is no longer just about payments—it’s evolving into a fully integrated financial experience. Open Banking, BNPL, and digital-first platforms are creating an ecosystem where financial services are seamlessly embedded into daily transactions.

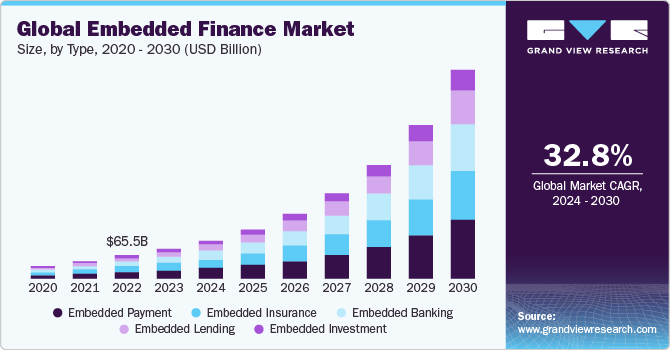

Global embedded finance market

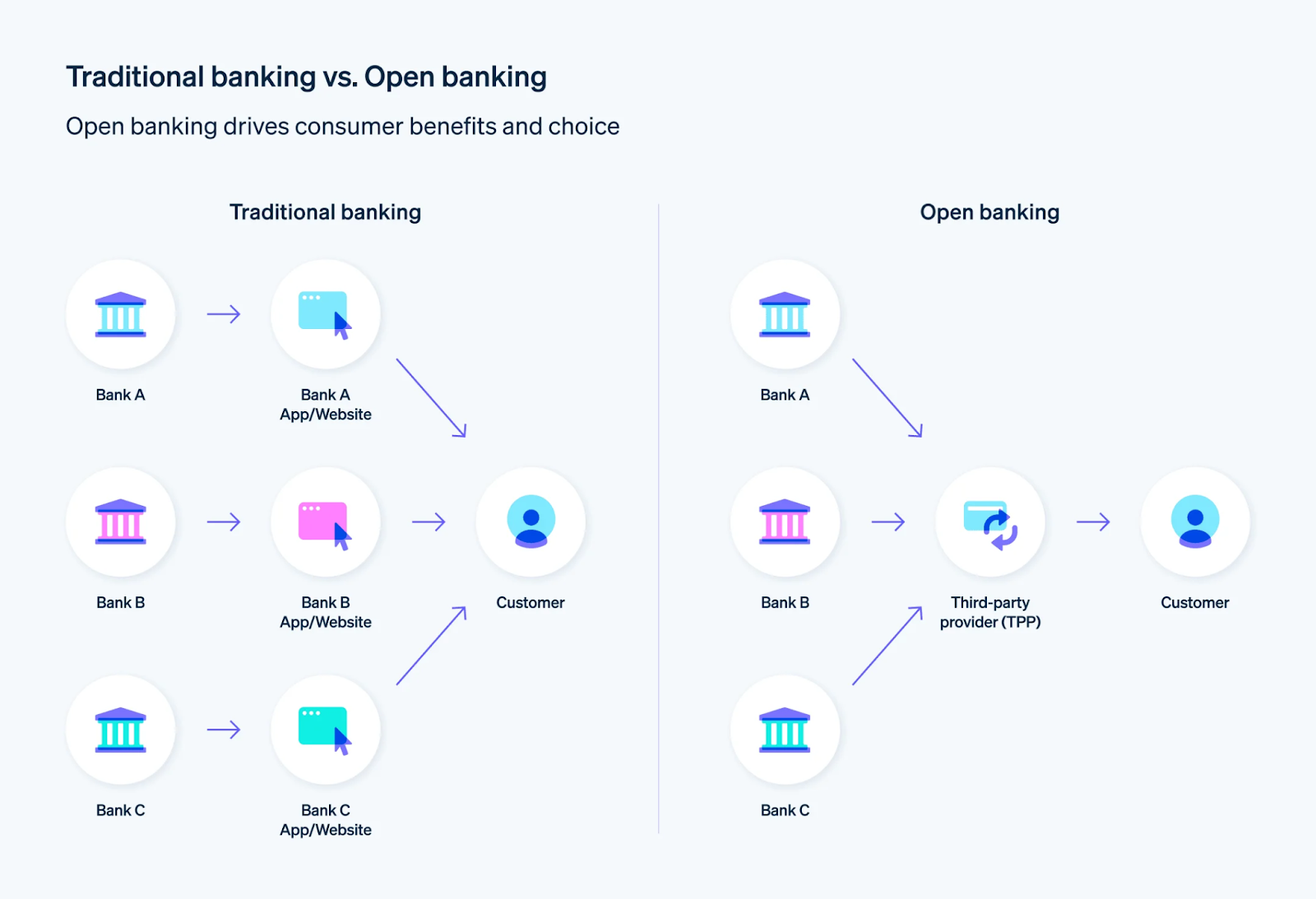

Open Banking enabling Embedded Finance

Open Banking has emerged as a critical enabler for the growth in embedded finance.

By making banking data easily accessible through the use of standardized APIs, open banking serves as a bedrock for interoperable and streamlined financial services.

It breaks traditional banking siloes and creates a secure and level playing field for third party services to integrate with multiple financial institutions.

Open Banking

With better access to financial data, non-financial firms can offer customized lending, insurance, and payment solutions—making Embedded Finance more scalable, personalized, and efficient.

Augmentum’s Backing

A) SME Banking

Embedded Finance is not just transforming non-financial industries. It is also redefining digital banking by integrating multiple financial services into a single ecosystem. A case in point is Tide. This Augmentum backed fintech firm (£2.0 million investment in May 2024) is embedding financial tools directly into its SME banking platform. With features like automated accounting, instant credit access, and payroll integration, Tide removes the need for SMEs to rely on multiple financial providers.

B) Consumer Tech commerce

Another, Augmentum backed, embedded finance use case is Grover, a leading consumer-tech subscription based platform.

Grover extends Embedded Finance beyond traditional BNPL by integrating asset-backed financing into its subscription model. Customers can rent devices, pay in installments, and access flexible ownership options, seamlessly within Grover’s platform.

Takeaway

With Open Banking accelerating financial integrations, we are seeing Embedded Finance expand beyond payments into lending, banking, and insurance. This transformation is making financial services more accessible, turning seamless finance into the new normal.

4) Regtech: Streamlining Compliance

Regtech (regulatory technology) can greatly help firms navigate the ever dynamic regulatory landscape.

Enablers such as AI, ML and big data are driving the adoption and effectiveness of Regtech. It allows firms to automate compliance and enhance risk management.

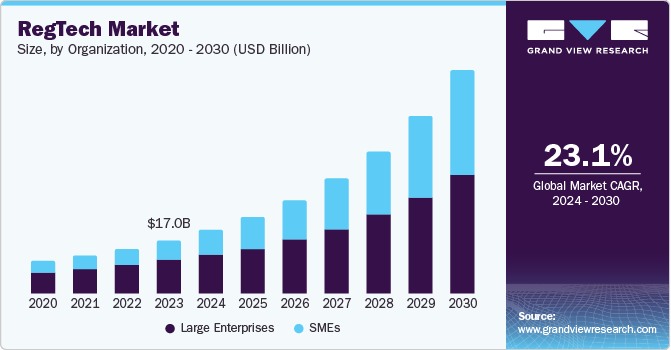

As regulatory complexities continue to rise, Regtech is experiencing exponential growth. Fintech firms are investing and are expected to continue investing in automating regulatory compliance and keeping pace with evolving regulations.

Regtech Market

Some Regulations driving complexity in Regtech

As governments and regulatory bodies introduce new and tighter regulations to address emerging financial risks and enhance consumer protection, regtech is emerging as a key enabler.

Some examples of key regulations driving the future of regtech include:

A) PSD 3 (Payment Services Directive 3) and PSR (Payment Services Regulations

PSD3 and PSR build on PSD2, making digital payments safer, smoother, and more transparent. While PSD2 introduced open banking across the EU, PSD3 takes it further by tightening fraud prevention, improving consumer protection, and enhancing cross-border payment efficiency.

B) EU AI Act

The EU AI Act seeks to regulate the development and use of AI by introducing a risk-based framework that categorizes AI applications based on their potential impact. The act aims to ensure AI is used safely, ethically, and without discrimination across industries including Fintech.

C) Evolving KYC and AML Regulations

Additionally the existing KYC and AML regulations are evolving to combat financial crime and enhance transparency, contributing towards an evolving regulatory landscape.

In the US, CTA (corporate transparency act) requires certain firms to submit beneficial ownership records. Similarly, in the EU, the new AML rules package seek to harmonise AML rules.

With increasing regulatory oversight, RegTech is transforming compliance from a manual burden into an automated, data-driven process.

Augmentum’s Backing

A notable example of this shift is FullCircl, a RegTech platform backed by Augmentum Fintech, which streamlines regulatory compliance for financial institutions. Its recent acquisition by nCino, (at a valuation increase of 80% for Augmentum) highlights the evolving importance of regtech in today’s financial ecosystem.

Takeaway

As compliance becomes both more complex and more critical, Regtech is emerging as a strategic differentiator—not just a cost center. Augmentum’s backing of FullCircl underscores its view that real-time, intelligent compliance will define the next generation of responsible fintech growth.

5) Payment Innovations and Cross-Border Transactions: Future of Global Commerce

The payments landscape is also undergoing a rapid transformation. Trends such as real time payments, open banking, and digital currencies such as CBDCs and stablecoins, are enhancing both domestic and cross-border transactions.

Some key trends driving payment innovations and cross-border transactions include:

A) Real Time Payments (RTP)

Real-time payments (RTP) are revolutionizing money movement by enabling instant, 24/7 fund transfers between banks, businesses, and consumers. While RTPs were initially used for urgent payments, they are now becoming mainstream and the new norm for transactions. The U.S. real-time payments market is projected to grow at a CAGR of 30.9% from 2023 to 2030, reflecting a global shift toward instant, frictionless financial interactions.

Some examples of RTP include FedNow (US), UPI (India), and SEPA Instant (Europe).

As demand for faster, cheaper, and more transparent transactions rises, RTP will play a pivotal role in reshaping payments.

B) CBDCs and Stablecoins

Another trend reshaping the payments landscape is CBDCs and stablecoins, leading to faster, more efficient digital transactions with reduced reliance on traditional banking networks. CBDCs, issued by central banks, provide a regulated, digital alternative to cash, improving financial inclusion. As adoption accelerates, CBDC transaction volumes are projected to reach 7.8 billion by 2031, signaling a major digital-first payment shift.

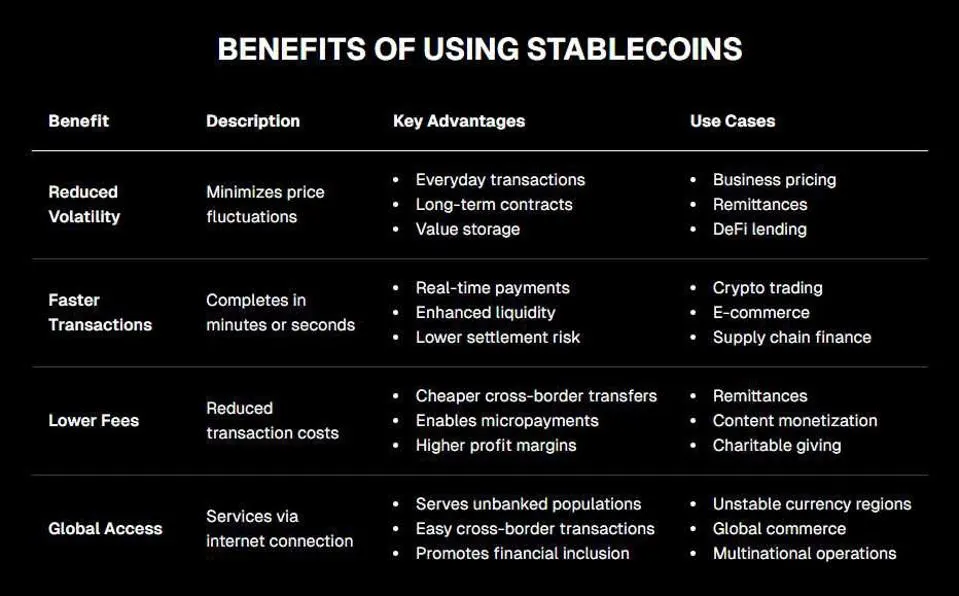

Meanwhile, stablecoins—cryptocurrencies pegged to specific assets or baskets of assets—offer price stability and a reliable medium of exchange. By reducing volatility, stablecoins simplify global commerce, enhance cross-border transactions, and provide a bridge between traditional finance and digital assets, offering a slew of benefits.

Benefits of Stablecoins

C) Cross-Border Transactions

As real-time payments (RTP) become mainstream and CBDCs and stablecoins gain adoption, cross-border transactions are undergoing a major transformation. Open banking is enabling seamless data-sharing, improving payment transparency and security. Meanwhile, alternative payment rails, such as blockchain and fintech-powered networks, are bypassing traditional correspondent banking, reducing costs and settlement times.

Augmentum’s Backing

Augmentum’s continuing investment in Volt.io, a provider of A2A payments connectivity for international merchants and PSPs (payment service providers) highlights Augmentum’s bet on evolving payment innovations landscape.

Takeaway

With real-time payments, CBDCs, and stablecoins streamlining transactions and open banking enhancing interoperability, the payments sector is becoming faster, more transparent, global, and seamless.

CONCLUSION

While these five trends are shaping the future of fintech, they are by no means the only forces driving innovation. The fintech landscape is evolving rapidly, with advancements in quantum computing, decentralized finance (DeFi), and tokenization poised to redefine financial services further. As technology continues to push boundaries, fintech will remain at the forefront of financial transformation, creating new opportunities and reshaping global commerce in ways we are only beginning to imagine.