Robo Advisory: Understanding from Service Provider’s Point of View

The idea of keeping investing decisions free of emotions has been around for a long time, but applying the same was not exactly possible because of human involvement. No matter how hard one tries, detaching biases from human judgment is almost unrealistic. On the other hand, a holistic understanding of the human condition is also vital for providing effective wealth management that can define advisory in its ideal state.

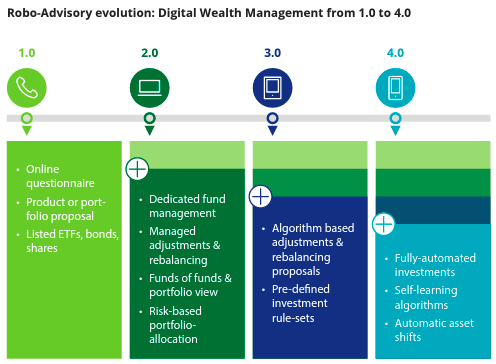

Robo advisors (RAs) are gradually bringing the benefits of AI and ML together. Robo advisors take on wall street by automating investment decision-making without emotional guidance, and that too at just 52% of human advisory costs. Although RAs came into being with more straightforward objectives, such as retirement planning to generate safe and optimal returns, their scope will broaden dramatically with technological advancements.

Source Credit: Deloitte

Let us look at the different robo-advisory models today and the value propositions they offer.

The various RA models

- White-label robo-advisory involves offering a provider’s technology and platform to other companies under their branding.

- Platform robo-advisory refers to a standalone platform developed and operated by a company for its clients.

- SaaS robo-advisory is a shared service where a third-party provider hosts and maintains the platform.

Robo Advisory as a white-labelled solution

As a product offering for the contracting partner, RA automates non-technical tasks such as customer onboarding, account opening, and account management. The bank retains ownership of all financial information on its clients’ accounts. At the same time, the service provider manages day-to-day operations such as creating new accounts, updating contact information, and being their asset custodian. This means a provider can offer their application to any company, large or small, and customize it to their needs. Automated reports are provided for each client, so they don’t have to worry about anything else but focus on what matters, i.e., maintaining client relations. SigFig, WealthKernel, and AdvisorEngine are examples of companies that provide white-label robo-advisory solutions.

Services offered by White Label RAs

- Providing insight into customers’ financial profiles and performing routine monitoring of accounts (such as analyzing balance trends)

- Identifying potential fraud risks through automated detection mechanisms

- Rebalancing portfolio automatically and customizability based on trade allocation rules, improving portfolio returns by .91%

- Maintaining customer data systems within their IT environment so that they can respond quickly without having to rely upon third parties like banks’ call centers

- Offering payment gateway support based on customer preferences

Attractiveness of white-labelling

White labelling is a great way to enter the market with brand differentiation and grow your business. There are some advantages to it:

- The white-label solution is considered the most uncomplicated variant since it does not require any changes in code or interfaces between the bank and the service provider.

- However, this type of collaboration requires high trust between both parties. Therefore, banks are only willing to use this method if they have enough resources for risk management and compliance issues related to this kind of cooperation.

- Banks can leverage a white-labelled solution without having the time or money to create an original product.

- Still, certain changes must be made per the bank’s requirements before launching your project.

Robo Advisory as a Proprietary Platform

This model of robo-advisory is built to direct services to individual investors without the involvement of any intermediaries. The platform can be accessed by the investors via mobile apps or websites. D2C robo-advisory firms such as Betterment, Wealthfront, and Personal Capital can support multiple RAs that serves as a comprehensive software solution for every kind of advisor or practice type (e.g., target-specific RAs).

Such RA platforms are essential to the private banking value chain as they help lure tech-savvy clients with their offering of personalized portfolios. Even HNI investors value seamless journeys amidst an omnichannel setting because it allows them to stay loyal to their banks. The evolving nature of client behavior and expectations is expanding the global RA user base, which is expected to cross half a billion by 2025.

The attractiveness of a proprietary platform

A standalone digital platform is more flexible, scalable, and secure than an RA application.

- It enables swift scalability of your business which is in tandem with the growing client base.

- The customer interaction benefits such as Wealthfront customer service are a USP of such platforms.

- Platforms can be way more reliable when built on the foundation of AI technology. It significantly enhances the processing efficieny of transactions and reports generation. In addition, platforms such as SoFi are usually more suitable to assist financial advisors in understanding their client needs, as the combination of technological sophistication and advisor contact is quite optimal.

- These platforms typically offer low-cost investment solutions, providing a user-friendly interface for investors to manage their portfolios. Moreover, as the adoption of the platform solution grows, transaction costs will further slash due to network effects.

Robo Advisory as a SaaS

In the SaaS model, a third-party provider offers the robo-advisory service. The provider hosts and maintains the technological infrastructure, while the clients access the platform through a subscription-based arrangement. As the platform is shared among multiple users, clients tend to have limited customization options. Institutional robo-advisory services such as betterment alternatives cater to institutional clients like pension funds, endowments, and other large-scale investors. These platforms offer tailored investment solutions and risk management strategies implemented by algorithms based on client-specific analytical data. BlackRock’s Aladdin, for instance, provides institutional investors with robo-advisory services proficient in portfolio management and risk analytics.

Attractiveness of SaaS

SaaS robo-advisory solutions offer cost efficiency, scalability, and integration capabilities similar to a white-labelled solution but with little to no customizability. Here is a list of advantages it provides:

- The solution consists of the necessary algorithms, data analytics tools, portfolio management functionalities, and user interface components.

- It’s a plug-and-play solution that often aligns with the client’s branding that extends a consistent user experience to their customers.

- The SaaS provider is responsible for handling server maintenance, upgrades, and security, which allows clients to focus on their core business.

- Integration with other financial tools and systems used by the client, such as customer relationship management (CRM) software or trading platforms ensures seamless data exchange capability.

- Compliance with relevant financial regulations and data security standards can be automated by SaaS robo-advisory providers in their platforms.

Robo advisory is more than a software solution

From a service provider’s perspective, RA is more than just a software solution. It is considered a prototype representing a decision support system from a technological viewpoint and a personal assistant from a product offering perspective.

Many hybrid RAs leverage technology for portfolio allocation and rebalancing while providing access to human financial advisors for personalized advice and support. One example is Vanguard’s Personal Advisor Services, its Robo review can be found here.

These are just a few examples of different robo-advisory business models. The financial industry has always been open to technological adoption, and the adoption of fully automated AI-driven software is an excellent example of this trend. RAs have come a long way from mere stock recommendation tools used by FIs internally to fully integrated investment platforms for retail investors.

The robo-advisory landscape continues to evolve, and various firms may adopt unique approaches based on their target market, value proposition, and technological capabilities.