FinTech Innovations and Regulatory Challenges in Insurance Industry

Insurance is a highly regulated industry. Most of the insurance regulations and legislations are made as suitable for the traditional business models of insurance. However, the endless technological innovations in the fintech space, specifically in the insurance sector are transforming its regulatory landscape.

Technologies like artificial intelligence, smart contracts, the Internet of Things (IoT), blockchain, machine learning, etc. are contributing hugely to the growth of the insurance business in today’s emerging market. Every area of insurance like marketing, customer service, underwriting, distribution, pricing, and products are infiltrated by the fintech innovations.

Balancing risk and innovation has become a great challenge for insurance regulators. New fintech insurance companies are also facing the challenge to keep up with the increasing compliance requirements. Though challenges can be turned into opportunities, regulatory changes take slightly more time than digital transformation. Let us explore the regulatory challenges in the insurance industry due to innovations.

- Consumer protection

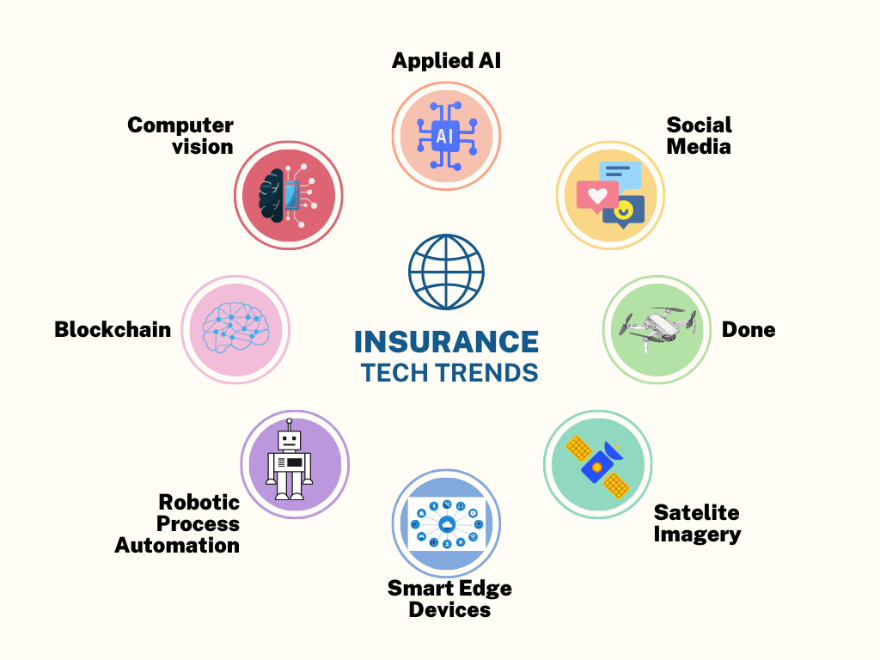

The insurance industry landscape is highly impacted by evolving digital technologies both in its operations and consumer-facing roles. Many of the fintech insurance startups that follow new tech-driven business models offer data-driven insurance solutions. They use various trending technologies for the collection and processing of consumer data. The following are the top emerging tech trends in insurance:

While these technologies give a seamless experience to consumers with faster processes and many self-service tools and platforms to use. However, many of the consumers may provide their consent without being aware of the types of data collected and the way it is used. Hence, data-driven insurance solutions pose a regulatory challenge in terms of consumer data protection. It has become imperative for regulatory bodies to set the applicable standards and regulatory measures for consumer data protection by assigning liabilities.

- Cybersecurity and data privacy

Data analytics using artificial intelligence and the use of third-party services for data collection brings in a huge challenge of cybersecurity and data privacy to the insurance industry. Cybersecurity incidents can lead to a huge loss for business and its reputation.

- Data Transparency

The usage of automation and algorithms in the insurance sector is extremely beneficial for customers in many ways for them to experience effortless insurance buying. However, automation and algorithms in insurance decision-making can lead to injustice as insurance companies can say algorithm-based forecasts are not explainable.

Insurance regulators are specific about data transparency in insurance. For example, Ontario’s regulator has shown concern over auto insurance rating models and is now looking into the outputs of AI-based black box models.

- Financial exclusion risk

With new ways of data collection through innovative technologies like big data and robotic process automation, insurance companies can understand customer requirements effectively, offer accurate pricing of risk, detect fraud instantly, and provide highly-personalized coverage. Though it is beneficial for many customers to get customized coverage at a reduced cost, the model can be susceptible to regulatory challenges as mentioned below:

- Some customer segments can face higher premiums through the granular method of data-driven pricing.

- Some customer segments can face a denial of insurance coverage which can lead to the risk of financial exclusion.

Insurance regulatory framework to boost innovation

Insurance regulators across the globe are also providing room for innovations by crafting regulatory frameworks for digital innovators. Here are a few examples of the same:

- The Financial Services Regulatory Authority of Ontario (FSRA) has Test and Learn Environments (TLEs) for financial services innovations. This approach is used for validating and assessing the new products, services, and business models of fintech insurance companies, specifically for property and casualty insurance, life, and health insurance.

- The Insurance Regulatory and Development Authority of India (IRDAI) has a Regulatory Sandbox Approach to provide a time-bound testing ground for new insurance products, business models, and applications.

- The Insurance Regulatory and Development Authority of India(IRDAI)has introduced ‘Use and File’ procedure to aid product innovations by permitting the general insurance companies to launch their new product without taking a prior approval from the regulator.

- This year, IRDAI has introduced new regulations on payment of commission. The regulator has made this changes to enhance responsiveness to market innovations, to help insurers to develop new business models, strategies, processes and to provide flexibility to insurance companies to manage their expenses.

How are Insurance RegTech Companies Reacting to Regulatory Challenges?

With the rapidly evolving insurance business models, increasing competition, and growing tech innovations, there is a need for insurance fintech startups to address the regulatory challenges by adopting new technology for regulatory requirements.

RegTech can play a crucial role in overcoming the regulatory challenges in the insurance industry. It can help insurance companies in meeting compliance requirements in a more efficient manner. Here is how RegTechs can help the insurance industry by embedding the regulations in insurance.

- Improve regulatory compliance

- Automation of complex compliance reporting

- Meaningful analysis of critical compliance areas

- Surveillance/monitoring of transactions

- Reduces reliance on third-party services

- Early identification of regulatory issues

- A complete view of compliance

- Regulatory automation can help in cybersecurity and risk management

Here are top 5 RegTech companies serving the fintech and insurance industry

| Company Name | Founded Date | Business Location | Estimated Revenue |

| Chainalysis | 2014 | US | $147 Million |

| Comply Advantage | 2014 | UK | $12.6 Million |

| CyberGRX | 2015 | US | $30.2 Million |

| Elliptic | 2013 | UK | $21 Million |

| Drata | 2020 | US | $63 Million |

Conclusion

Various regulatory reforms being introduced by the insurance regulatory bodies across the world would aid product innovation, boost ease of doing business, make insurance distribution networks stronger,enhance customer experience with reduced cost and streamlined processes. A flexible regulatory framework and the adoption of emerging RegTech solutions by insurance fintech companies can be a great way to keep up the insurance innovation. Overcoming regulatory challenges can create a safe, competitive, stable, and customer-centric digital insurance ecosystem.