Challenges Banks Are Facing To Implement Blockchain Technology

Blockchain technology is a decentralized, distributed ledger system that records transactions across multiple computers, ensuring that data cannot be altered retroactively without altering all subsequent blocks and gaining consensus from the network. Implementing blockchain technology has the potential to transform banking, offering greater transparency, security, and efficiency in financial transactions. Read some key advantages of block chain technology in banking here.

Despite the global blockchain in the BFSI market estimating a CAGR (Compounded Average Growth Rate) of 73.8% between 2019-2026, the technology continues to face challenges e.g. – in China, Qatar, Algeria, Morocco and Tunisia.

No matter how efficient a technology is, there are often other factors that restrict its adoption. A World Economic Forum report of 2016 reported that 24+ countries’ interest in distributed ledger technology (DLT) and More than 90 central banks are already in this discussion.

In this report, we will understand seven key challenges that the banking industry and economies are facing while implementing blockchain technology, but before that, it is essential to go through the regulatory situation around the globe.

Explanation Of Regulatory Situation Worldwide

While talking about blockchain, no one case escapes the topic of cryptocurrencies. The countries that are regulating cryptocurrencies are effectively reaping the other features of blockchain technology as well, like a distributed ledger.

Roots of Bitcoin

The usage of blockchain technology has been prevalent since the origin of “Bitcoin” in 2009. As digital currency seized the limitations of fiat currency, it caused the need to implement the former. Since Satoshi Nakamoto prevailed in Japan, the roots of smart contracts were already laid there. Likewise, in 2017, the Tokyo government adopted “Bitcoin” as a legal currency. Later, as years passed, other nations like the United States adopted blockchain technology.

Japan was one of the acceptors

Moreover, as of (link 6) the Payment Services Act of 2019, even the Japanese government has recognized crypto assets as legal. The Financial Services Agency (FSA) has passed two laws on rules, procedures, and token offerings on crypto offerings. It includes Japan Security Token Offering Association (JSTOA) and Japan Virtual Currency Exchange Association (JVCEA).

How the US Reacted to Japan’s Acceptance of Cryptos

Various federal regulatory agencies have supported the intervention of blockchain technology in the United States. According to the Commodities Futures Trading Commission (CFTC), cryptocurrencies like Bitcoin, Ethereum, and others are already regarded as “Commodities.” Likewise, crypto platforms like Coinbase and Binance are also considered legal. As per the Bank Secrecy Act (BSA), financial institutions like banks must report payments to the federal government.

Other nations are on their way

Similarly, other nations also introduced blockchain technology in banking, which includes Portugal, Singapore, United Arab Emirates (UAE), and the United Kingdom. The application of crypto and blockchain technology is visible in the payments, remittances, and settlements arena. With the help of smart contracts, the transaction speed is reduced to seconds.

As a result, banking services also become quick and secure. The involvement of blockchain provides ease in accounting treatment, digital verification, and faster payments. Any intermediaries or hidden fees disappear within the process. At the same time, instead of KYC (Know Your Customer), digitized fingerprints or security keys could be used.

That being said – according to a report, as of 2023, while there are more than 420 million crypto users – it is still a tiny portion of the 8 billion total population worldwide.

Pie chart of the population

Despite increasing awareness and acceptance, there are a few challenges that the BFSI sector is facing while implementing blockchain technology.

These challenges are as follows-

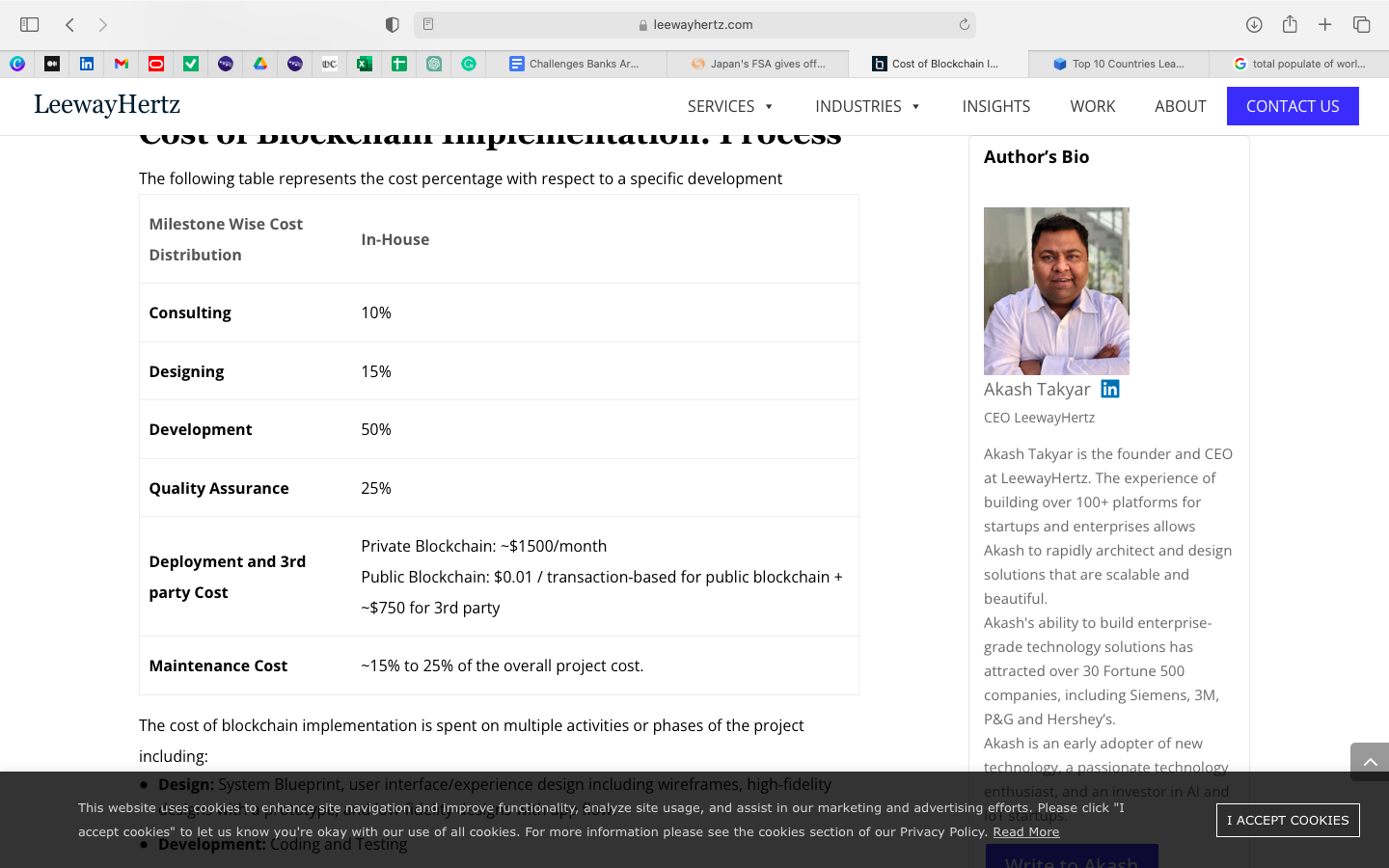

Cost and Maintenance

Although the need for papers and receipts reduce, there is a similar amount of maintenance required for blockchain technology. Huge graphic processing cards (GPU), software, and hardware are required at the initial phase of launch. In the absence of these, the whole blockchain system can fail.

If financial institutions wish to develop a blockchain platform, the cost ranges from $30,000 to $300,000. Likewise, it might take 9 to 10 months for its development. Plus, the maintenance for the entire system needs almost 15-25% of the total project’s cash flow. In addition, validators incur a huge electricity power cost to verify the transactions. Thus, small and emerging banks cannot complete this space considering their sustainability in mind.

Diversified authority of control

Diversified authority of control in blockchain technology refers to the decentralized nature of the technology, where multiple participants have equal authority and control over the system. It can be a challenge for the banking sector in the process of adapting and implementing blockchain technology because the traditional banking system is highly centralized, with a few large institutions having control over most financial transactions. In short, the authority will shift from financial institutions to validators. Every participant involved will hold equal rights. So, the latter will confirm the payment transactions.

Scalability Issues

Scalability could be the major issue in the case of blockchain technology implementations as the study of Cambridge University states that the current global energy consumption of the Bitcoin network is around 121 terawatt-hours per year, which is equivalent to the energy consumption of Argentina.

Let’s understand this more; it involves maintaining a distributed ledger of transactions which are connected across the network of nodes. As the number of transactions increases in nodes and networks, the requirement of storage and amount of computational power also increases.

One of the best-known blockchain networks, Bitcoin, has been struggling with scalability issues for many years. The Bitcoin network has a block size limit of 1 MB, which limits the number of transactions that can be processed per second. It has resulted in long transaction processing times and high fees during times of high network activity.

Similarly, the Ethereum network has also faced scalability challenges, with the network becoming congested during times of high demand. This congestion has led to slow transaction processing times and high fees.

Lack of Abundant Expertise

Blockchain technology involves complex installation. Very few individuals in the financial and banking industry can understand smart contracts. Its development needs professionals and technical staff to handle the system. Plus, the mining and validation process involves huge processes. Therefore, a lack of knowledge about this technology can cause a severe challenge to banks.

Technical Complexity

Blockchain technology does not allow a centralized power to control its operations. Instead, there is equal and transparent distribution of data. However, for banks, it disrupts as millions of customers take their services. As a limitation, blockchain technology lacks a robust security system. There are equal chances of fraud, KYC, and Anti-Money Laundering (AML) issues.

Since the blockchain ledger is visible to everyone, anyone can view the transaction.

With both keys distributed, the private key stays with the user, and the public key is on the blockchain. The former gives a chance to the hackers to disrupt the entire system. For example, several banks that involve blockchain as a part of transaction processing cannot store them in their system. So, if a person has $1 million in his account and transacts $75,000, the validators (probably anyone) can view the receipt. As a result, the complexity also increases.

Regulatory Challenges

Not all economies are allowing blockchain technology to operate due to various reasons, and one of the primary reasons is speculation behind cryptocurrency. The challenges backed by various regulatory bodies significantly impact the banking sector. According to a US (United States) bill passed, which was passed in February 2022, the New York government has allowed records, signatures, and the use of blockchain technology in various smart contracts.

However, in 2019, the popular cryptocurrency platform “Binance” was banned in the United States. Countries like Bolivia, Egypt, China, Columbia, Turkey, Iran, and others have restricted the use of blockchain. As a result, it has caused severe regulatory roadblocks for the overall acceptance.

Interoperability Challenges

In the banking sector, interoperability is especially required due to various transactions between the accounts in the same bank and interbank as well. It requires different nodes to perform seamlessly, which is supposed to be faster than traditional banking systems.

One challenge with blockchain interoperability is that different blockchain platforms may have different consensus mechanisms, data structures, and smart contract languages, which can make it difficult to transfer data and assets between them. It can create data silos, where information is stored on different blockchains and cannot be easily shared or accessed.

Another challenge with blockchain interoperability is that it requires a high level of standardization and collaboration among different blockchain networks. It can be difficult to achieve the banking objectives, as different blockchain networks may have different goals, incentives, and governance structures.

Conclusion

When a technology is introduced by any country, it doesn’t only help a particular country to enhance their operations and economic security, but also helps businesses all over the world to step up in wealth creating businesses. Blockchain technology is one of the most revolutionary technologies to establish a sense of security and fast processing infrastructure for corporations.

Moreover, financial institutions are the base of any economy which has to be covered with the fastest and latest technology which provides security, decentralization and quick operations. Blockchain technology could be the best possible way to enhance the end customer satisfaction by giving them quick access to their funds, minimal requirement of documents every time they make transactions and much more.